Eurobond market: why OFAC's license non-renewal after May 25 is not a big deal?

The U.S. Treasury Department’s Office of Foreign Assets Control is expected to let a temporary exemption authorizing Russia to pay bond coupons lapse once it expires on May 25, people familiar with the matter told Bloomberg. The waiver allows US investors to receive payments from designated entities (including the Bank of Russia, the Russian Ministry of Finance and the NWF). After May 25, U.S. banks will not be allowed to process payments to U.S. residents.

They will have to apply for individual licences to receive payments from designated Russian entities. The news triggered a new wave of fears of an imminent technical and then real default on Russian sovereign bonds. Russia’s state bonds tumbled 5 to 12 pt overnight. Therefore, almost all securities or Russian entire sovereign yield curve have dropped again to prices seen in early March.

A good buying opportunity We believe the current prices are extremely attractive for bond purchases, while the current discount fully covers possible risks. Russia’s next debt transfers (totalling $99 mln which is negligibly small even compared with the daily export revenues) on foreign bonds maturing in 2026 and 2036 are due on May 27 that is after the OFAC license expiration. However, we expect that the obligations will be successfully fulfilled in any case.

Is a default unlikely? The speculations about sovereign default risks had weighed on the markets earlier. On April 5, against the background of another geopolitical escalation, the US Treasury suddenly cut off Russia's access to the frozen funds it used to make coupon payment in March. The move was meant to force Moscow to use its holdings of dollars (a rouble payment would have constituted a default).

However, at the end of the 30-day grace period, the Finance Ministry made a payment in dollars and averted a real default by structuring the payment through non-sanctioned entities. JPMorgan, the bondholders' settlement bank, processed the payment.

So what should we expect after May 25, if the carve-out is not renewed, will Russia inevitably face a sovereign default in that case? The probability of a favourable scenario is at least 75%, according to our estimates. Despite recent pledge by Finance Minister Anton Siluanov that Russia intends to service its foreign debt in roubles (incidentally, the prospect of the Russia 26 issue provides for such an option), we have reasons to believe that on May 27 (and subsequently, if successful) the ministry will again use the scheme with payment through an non-designated agent that has a foreign currency account of the ministry. According to the payment order, the funds in the currency of the issue are subject to distribution between the National Settlement Depository (for local holders) and Euroclear. In other words, the cumulative funds will be sent to the overseas depository, which will be authorised to distribute it among the bondholders.

Will everyone but US investors receive the funds? Since the OFAC waiver does not impose any limitations on investors outside the US, they are very likely to receive the coupon payment (assuming the European banks do not stop the transaction on the pretext of compliance policy).

U.S. banks would probably not be able to process the payment and U.S. holders would not receive the money. The debt obligation is usually deemed fulfilled once the funds are credited to the lender's account. Therefore, U.S. investors may initiate a default procedure following a 30-days grace period. In this case applications from 25% or more of the bondholders are required.

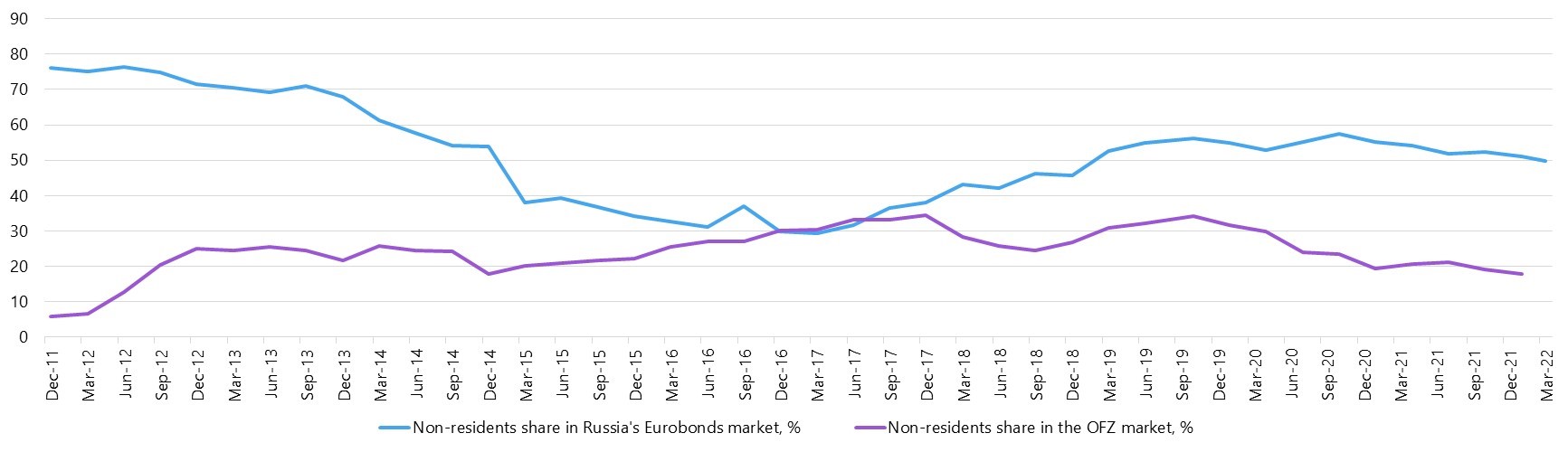

Change in the ownership structure of Russian Eurobonds

Given the sell-off seen at the end of March and the legal ban on holding Russian assets, we doubt there is a quorum for such a procedure (although we cannot be absolutely certain due to the lack of up-to-date data on holders).

We believe that major holders of Russian external sovereign bonds are European legal entities with Russian roots and European funds, which the Central Bank qualifies as non-residents as they hold securities in Euroclear. This also explains why the non-resident share in the Russian Eurobonds holdings (external debt) fell by just 1.3% to 49.8% in the quarter ending on March 31, according to the latest data from the Bank of Russia.

U.S. funds like T. Rowe Price, Blackrock account for less than 10% of the outstanding Russian sovereign bonds (according to Bloomberg data as of the end of April). Traditionally the largest holders of Russian external sovereign and corporate debt, including the financial sector, have been major European funds, with U.S. investors in second place and Southeast Asian (SEA) investors in third place.

The implication is that the non-renewal of the licence would above all hit US investors. Therefore, it cannot be ruled out that the carve-out will be extended after a while.

The bottom line is that the actions and statements of the US administration add pressure on Russian hard currency sovereign bond prices and set off a new wave of fears of an imminent default. However, Russia’s Finance Ministry has successfully tested a settlement scheme (and has access to the necessary funds) to make bond payments bypassing the restrictions without violating the terms of the issue.

Given that most of foreign holders of Russian bonds are investors outside the US, they are unlikely to seek to interfere with the scheme. Thus, Russia will proceed with coupon payments, while those blocked from getting money from the Russian sovereign will not be able to meet a quorum requirement to initiate litigation as part of default procedures. These considerations make Russia’s cheap sovereign Eurobonds even a more attractive investment asset.

Ownership structure of Russian sovereign debt

Source: Bloomberg, ITI Capital