The revival of Russian Eurobond primary market

Рынок Акций

Рынок Облигаций и Валюта

- The arrival of spring was marked by stronger demand for EM assets due to reverse in $ rate hike expectations and relaunch of global stimulus 2.0 worldwide. Primary external borrowing market in EM has started to rebound, as corporates line up new issues following a prolonged pause despite lingering geopolitical risks

- We estimate that only corporates issues could top $11 bln this year, roughly the amount seen in 2017. The projection does not reflect EM FX volatility and tougher US sanctions that could hit OFZs and erase the demand for new debt

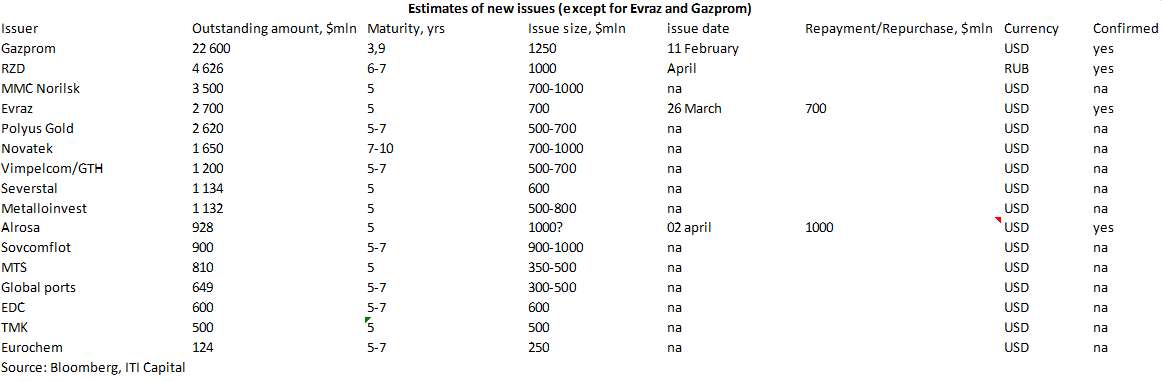

Corporates opened eurobond books

- After Gazprom’s successful placement in February and Russia’s sale of $3 bln 2035 and € 750 mln 2025 bonds, a window of opportunities opened up for other companies, suggesting sovereign risks are no longer there

- Unlike sovereign issues placed almost every year, given MinFin’s $3 bln external borrowing plan, the latest corporate issue were placed 12m ago in February 11, 2018 (Gazprom); January 25, 2018 (Rusal) for $500 mln maturing in 2023, January 24, 2018 (Polyus Gold) — $ 500 mln, $500 mln (Phosagro) and then only in November 2017

- The Eurobond market appears dried-up due to sanctions risks and higher risk premiums, that soared to 110 bps in early August before tumbling to 20 bps today

- Evraz was the first corporate to tap a debt market this year after the sovereign placement, except for Gazprom’s Swiss francs placement. Alrosa is planning 5Y placement in USD today

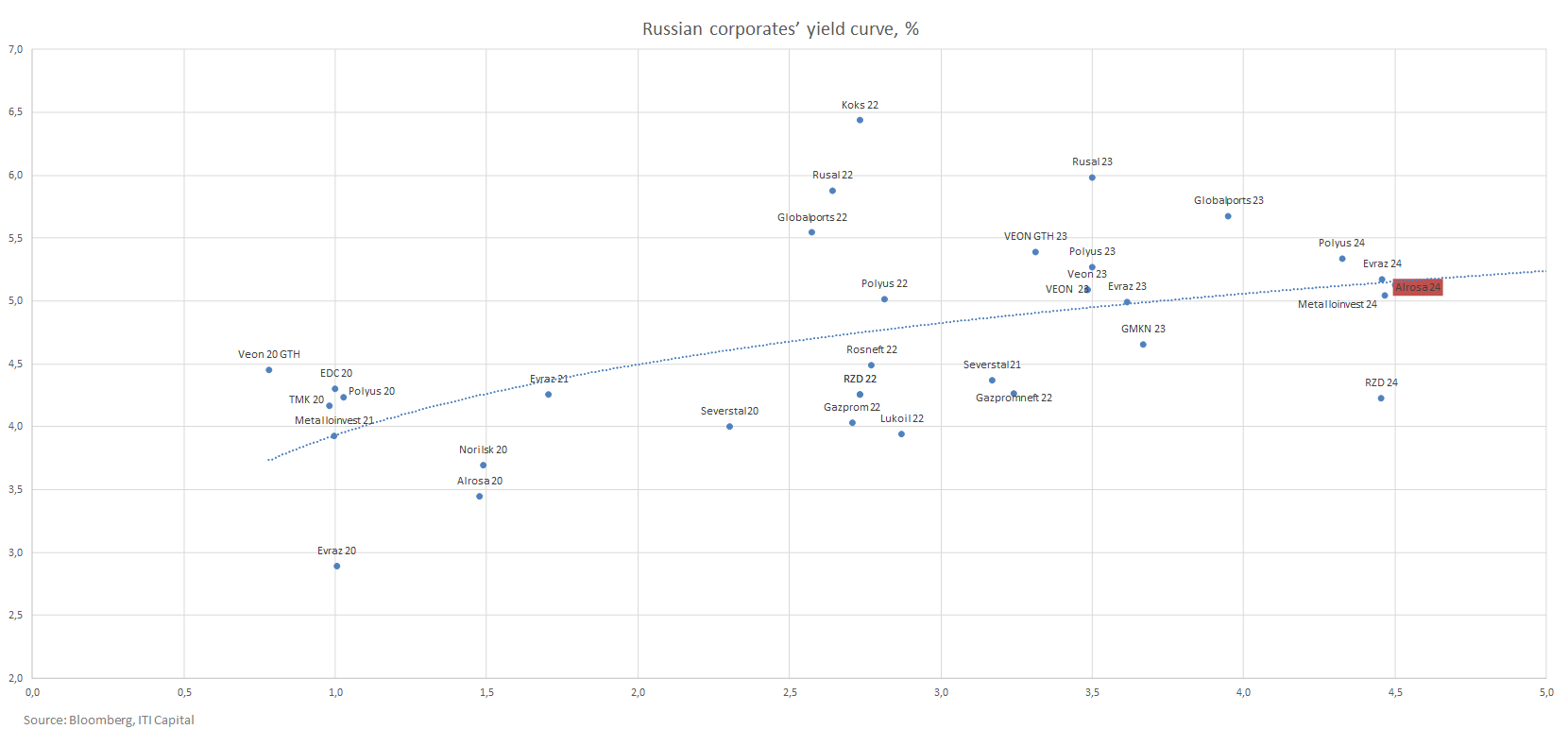

- We think that indicative yield of 5-5.125% is not very attractive offering 20-30 bps premium at most to existing yield curve. The premium has been falling as new issues emerged which is not very good amid EM volatility

- Most of the issuers that announced placement recently had borrowed overseas as long ago as in 2017. Alrosa announced a 5Y bonds placement to buy back $400 mln of 2020 maturing bonds

- Paying off short-term debt with a longer-term loan, as it is the case with Evraz and Alrosa, is the main reason behind debt placement. What is more, the placement allows the issuer to develop new benchmarking on the yield curve

Corporates issues could top $11 bln in 2019

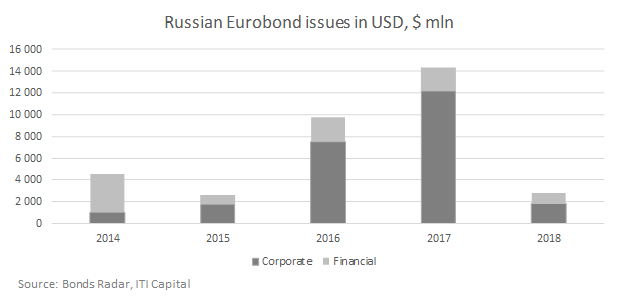

- According to our estimates the bonds sale, excluding financial sector and sovereign bonds, may reach $11 bln. The market is expected to be dominated by Russian issuers from metals and mining sector, given shorter duration (up to three years) of their issues and a long pause in placements that were held two years ago in second half of 2017

- During the peak placements in 2017, in USD, companies sold $14,3 bln of bonds, out of which $12 bln were dollar-denominated corporate securities and $2,1 bln finance. In 2018, the amount of placements shrank fivefold. If all those (corporates, including banks) willing to sell debt succeed, the cumulative dollar placements may surpass those of 2017

Russian issuers offer generous terms

- EM spree is fueling demand for risky assets and offering opportunities for the Russian issuers, as the key global central banks ease policy and cut key rates, bolstering markets amid rising slowdown and recession risks, particularly in Eurozone and EM (mostly in LATAM)

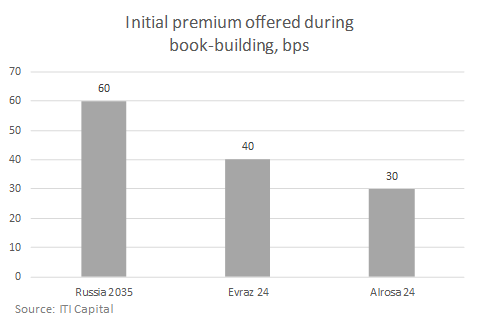

- Given the latest placements, the issuers, even Russia’s MinFin (2035 bonds) are offering a strong premium to the curve. When it comes to recent placement of Evraz, at time of issue the premium exceeded 30 bps during book-building, implying an upside price growth potential of 1% against par value, however demand was offset by EM turmoil. If the premium remains strong during book-building, as it was the case with Evraz (the book was oversubscribed three times), the market will continue to see surplus demand for securities issues by many corporates

- We believe that issuers are offering a generous premium, given the upside potential for many dollar-denominated corporate issues — not more than 0.5% on the long curve, or 10 bps yield decline, if they come back to pre-sell-offs levels (August); and 2% price rise and 25–30 bps yield decline, if they come back to pre-April levels (Rusal sanctions)

- Our forecast does not reflect sanctions and global correction risks. These risks increase every day due to significant overheating on the emerging markets and poor economic data