New Russia 2035 tranche looks appealing

Рынок Акций

Рынок Облигаций и Валюта

The Russian Finance Ministry has opened the order book for two tranches of Eurobonds: a new 16-year dollar issue and an additional euro issue maturing in 2025. IPT (initial guidance) for the dollar tranche is 5.5% and about 2.625% for the euro tranche.

New Russia 2035 tranche looks appealing

- The ministry reportedly plans to tap the market with $3bn placement, – euro-denominated issues would amount $1 bln, dollar-denominated issues are seen to limited to less than $2 bln. The previous eurobonds placement worth $1.5 bln was made back in March 2018. Tight market is fuelling appetite for high yield assets despite geopolitical risks. The Russian eurobonds outstanding amount to $33 bln and €1.8 bln

- Given the high premium to the curve of about 60 bps, the final dividend will not yield above 5.2%. Excess demand is expected to slash the premium by half, to 30 bps, from indicative 60 bps as of today

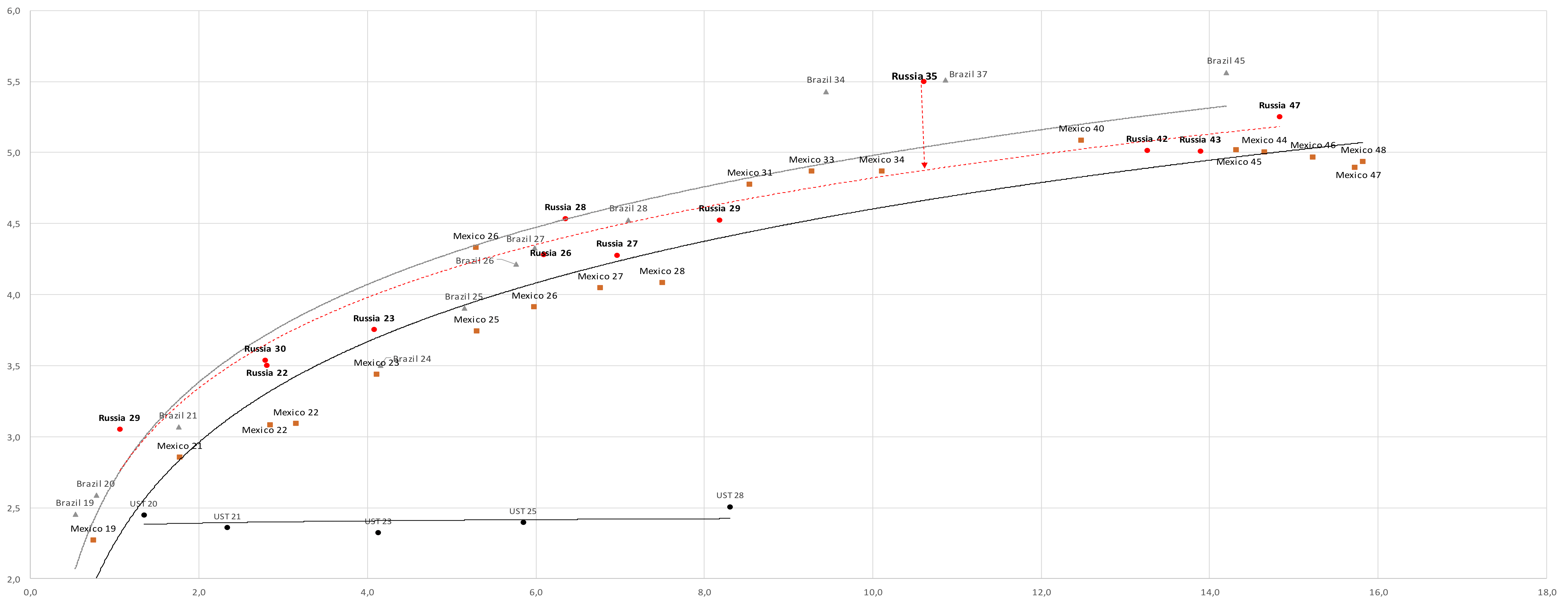

Russia, unlike Brazil, looks undervalued, as reflected in the country risk premium

- 5.5% indicative yield corresponds to BB-rated Brazil 34, which is four steps behind the Russian sovereign rating. On the sovereign side, the spread between Brazil and Russia has narrowed to a minimum of 5 bps against 50 bps on average, since Russia yields should be way lower

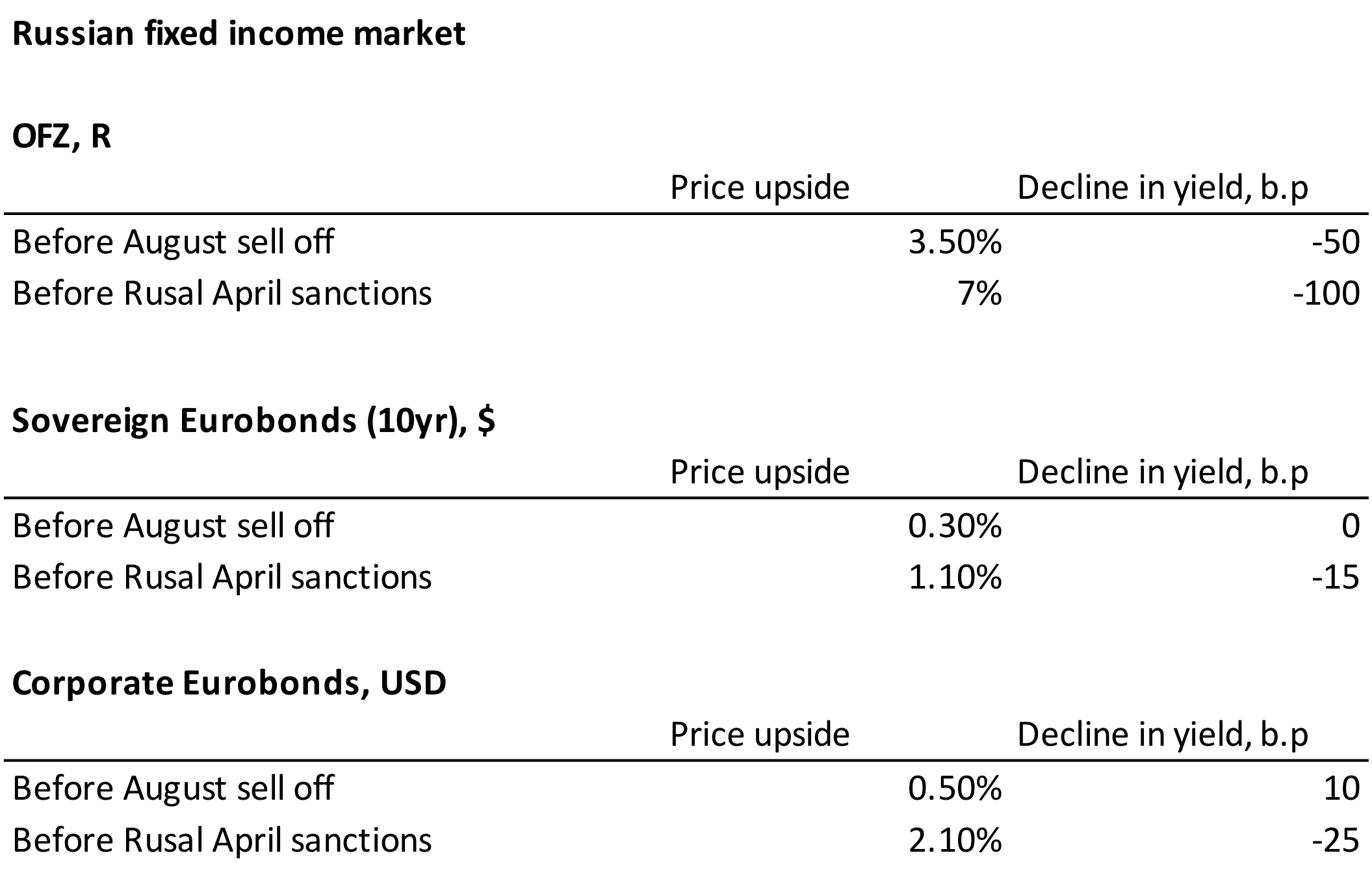

- The Russian curve has narrowed by 40–50 bps year-to-date and is trading at the levels seen at late July prior to sell-offs in August. Hence, the risk premium has dropped by 80 bps from November peaks, but its downside potential is limited due to sanctions risks. The current risk premium is only 15–20 bps above the level seen prior to sanctions against Rusal, while Russia 5Y CDS which is only 10 bps above the pre-sanction level

Source: ITI Capital, Bloomberg

Minfin external debt borrowing program, $ bln

Source: ITI Capital, Bloomberg

Russian and LATAM Sovereign yield curve, %

Source: ITI Capital, Bloomberg