Russia: CB cut the rate by 50 bps, making official shift to dovish monetary policy

Рынок Акций

Рынок Облигаций и Валюта

Key takeaways

- The CBR has cut the rate by 50 bps, to 5.5% (the lowest level since before 2014 sanctions) and will continue further easing, officially shifting from neutral to dovish policy despite the risks of an inflation pick-up this year due to the rouble weakness.

- We believe that after a bigger than usual 50-bps cut the CBR will continue monetary easing with gradual cuts in line with our estimates, bringing official benchmark rate to 4.5% by the year-end.

- The CBR’s rate policy will depend on factual and expected inflation, macroeconomic trends and global volatility.

Impact on markets

- Yields on the long end of the curve dropped by 10-12 bps, implying a 1 pp price growth. The rouble rallied by 1.2% to 74.24 per dollar.

- We think that at the current oil prices the Russian rouble is overvalued vs USD, which means there’s an opportunity to OW USDRUB.

- Russia’s current real rate has declined to 3%.

The key reasons for a shift in monetary policy

- Stabilisation of global financial markets since March

- Significant economic risks for Russia and global economy implying disinflationary pressures due to fading consumer demand which will offset temporary inflationary spikes as a result of the rouble devaluation due to a slump in oil prices

- The CBR is concerned that a slump in household disposable income may increase disinflationary pressure

- Recent increase in inflation expectations will be offset by a drop in consumption

Our take

The Bank of Russia has cut the key rate by 50 bps to 5.5%, sending a dovish signal to the markets. Bank of Russia Governor Elvira Nabiullina said another percentage point of interest rate cuts is possible in 2020. Such tone is clearly extremely positive for the rouble debt market, which immediately went up. The current OFZ prices do not yet reflect a possible rate cut to 4.5%, so we expect a bonds purchases ramp-up in the near future.

The new parameters that were announced last Friday by the CBR are very close towards our estimates from an inhouse macro model that we published a week before the CBR release.

Below are the key highlights from the press conference:

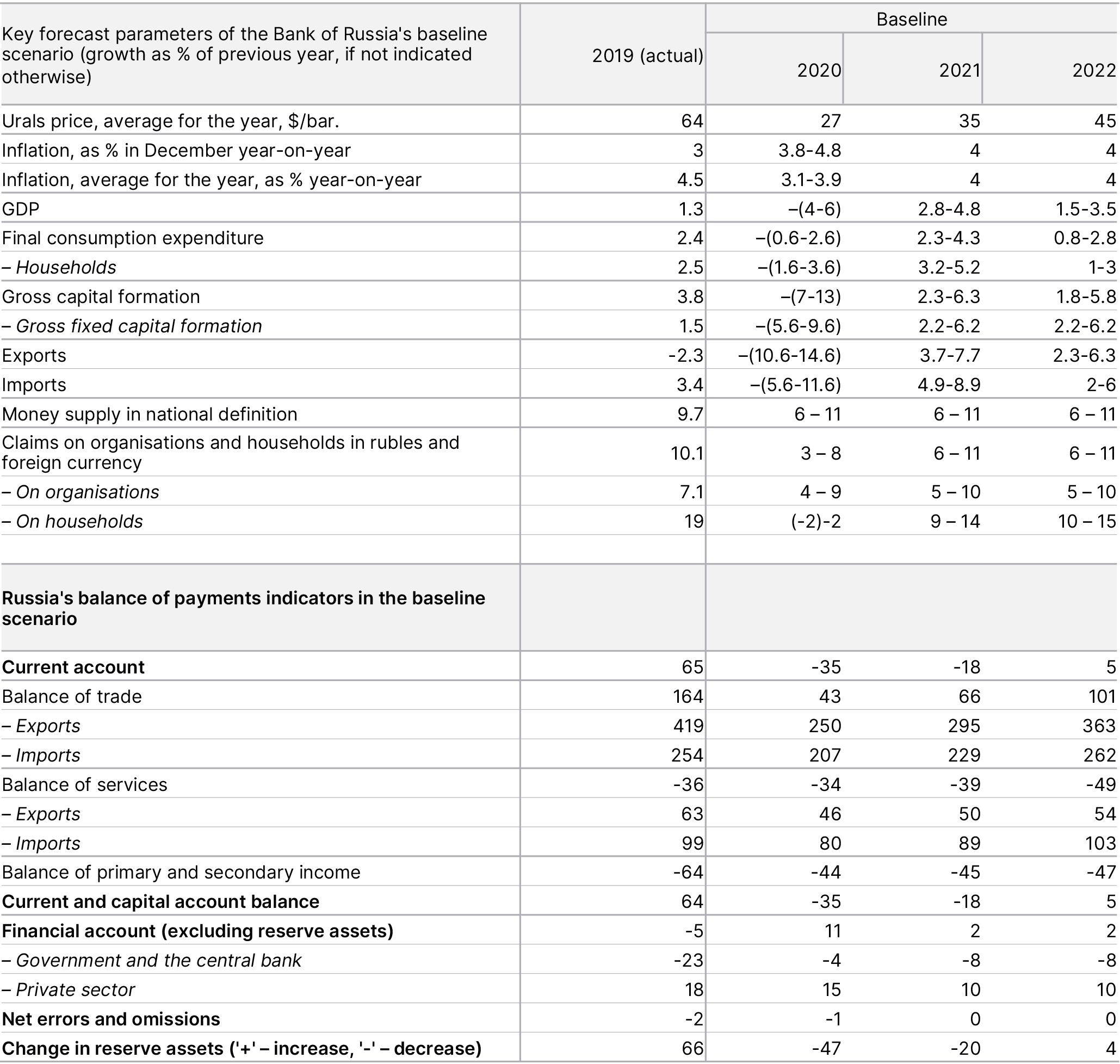

- The Bank of Russia has substantially reviewed its baseline scenario parameters. The forecast was reviewed due to such important factors as the global economic downturn, oil rout and restrictive measures around the world.

- Against this backdrop, the CBR has adjusted its macroeconomic forecast for 2020 and beyond. The regulator put a conservative view on oil prices in the forecast. The CBR assumes oil prices slow increase from an average of $15/bbl in the second quarter to $24/bbl in the fourth quarter. The CBR's baseline scenario now assumes an average annual price for Urals crude of $35/bbl in 2021 (instead of the $50 it predicted in February) and $45/bbl in 2022 (in place of its previous prediction of $50). Russia’s GDP will reduce in annual terms at least until the 3Q20, when a gradual economic recovery may begin, and the GDP may grow q-o-q. Russia's 2020 GDP is forecast to decrease by 4-6% primarily due to the decline in exports and capital investment. GDP growth is seen at 2.8–4.8% in 2021.

- The regulator expects that annual inflation will amount to 3.8–4.8% in 2020 and will stabilize near 4% in the future (the CBR’s target).

- CPI growth is projected to slow down amid disinflation factors. There’s a high probability that the CBR’s inflation control will help Russia avoid stagflation.

- Developing the monetary policy, the CBR will rely on the leading indicators, rather than the upcoming statistics. Due to the extraordinary conditions, the regulator has act more decisively. Thus, it reasonably switched to a wider-than-expected cut. Pre-emptive steps will also be taken in the future to normalize the situation. It cannot be ruled out that the CBR will deliver yet another 100-bps cut (bringing the rate to 4.5%) by the year-end. Therefore, another cut, which is seen more likely, will coincide with lifting the lockdown (to drive demand). The range of the neutral rate, in turn, will not be reviewed yet, and a wider range is not likely to hamper dovish monetary policy.

- The CBR expects that the current account balance will decline to negative values in 2020 (to -$35 bln) and return to positive territory on the back of projected export recovery. Russia’s budget deficit may amount to around 6% of GDP in 2020 amid lower revenues and higher stimulus spending.

- The CBR expects household disposable income to decline by 1.6-3.6% and savings to fall by 7-13%.

- The Central Bank expects capital adequacy ratios for commercial banks to drop to 3-8% from 10% in 2019.

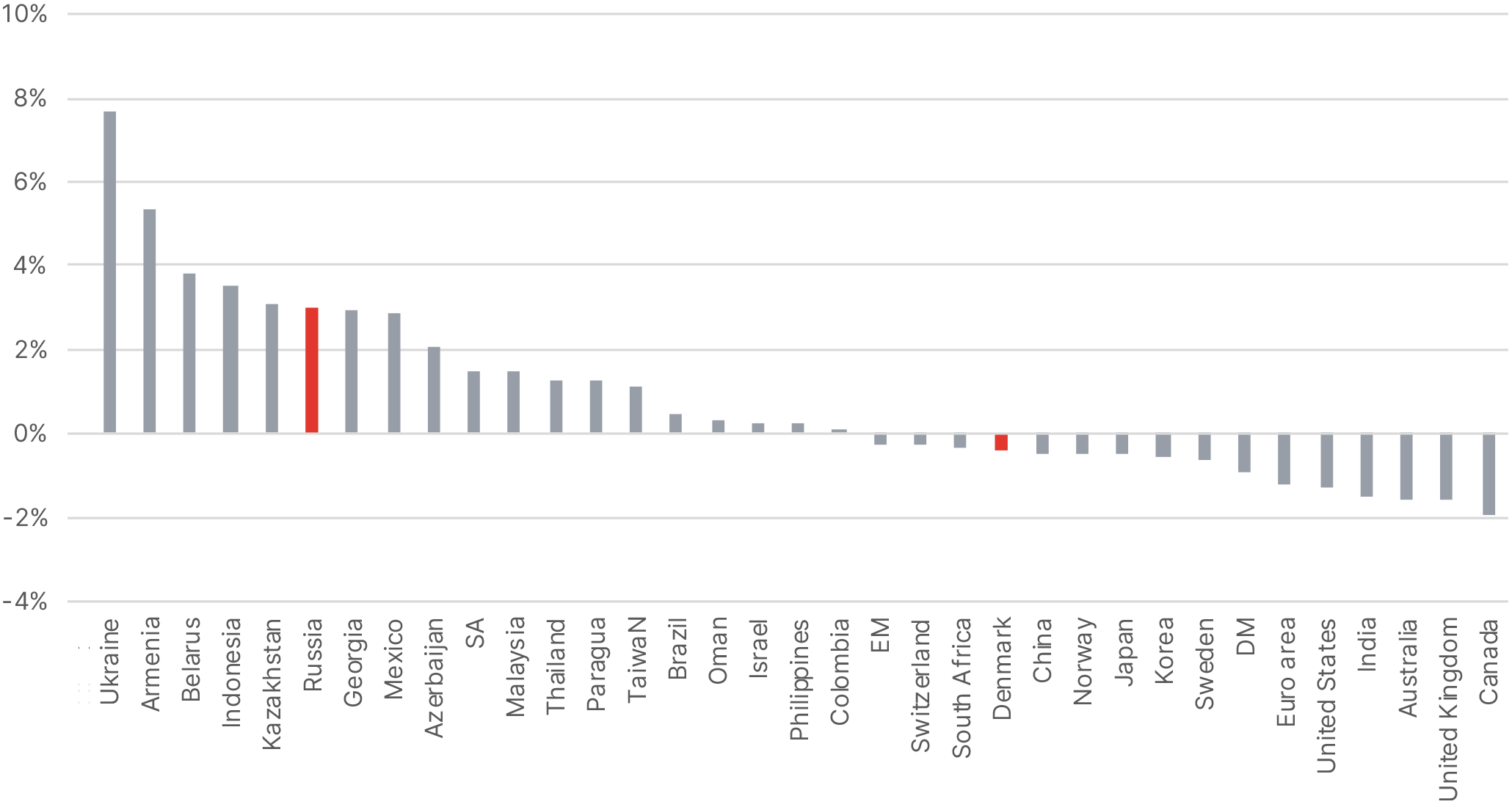

Real interest rate in local currency, %

Source: Bloomberg, ITI Capital

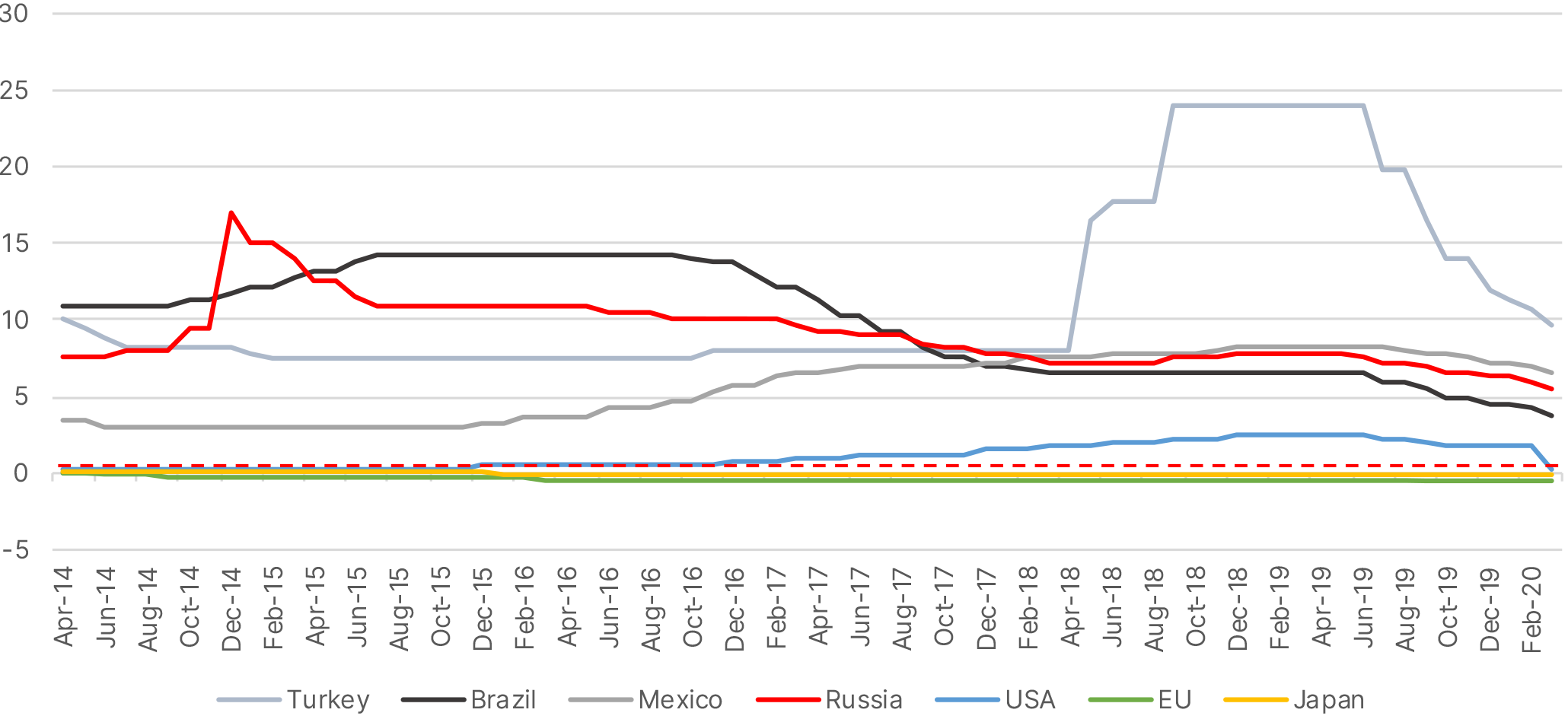

Global central bank rates, %

Source: Bloomberg, ITI Capital

Bank of Russia’s medium-term forecast

Source: Bank of Russia