Geopolitics and new opportunities in the Russian financial market

Diplomacy will prevail

We believe international investors are more skewed to harsher sanctions against Russia pushing Russian 5yr CDS at one point to pandemic highs (210 bps) and close to levels of 2014 sectoral sanctions (250 bps) despite Russia’s much stronger economic and credit fundamentals and support from the global commodity market. Before the pandemic, the cost of a five-year hedge against Russia’s default, or a five-year CDS, did not exceed 60 bps. We believe that both sides, the US and Russia, approached a red line and are not willing to cross it given huge consequences, so they are likely to try to step back and intensify negotiations, which they did on Tuesday 19 January. Tuesday's selloff in Sberbank shares seemed more like a margin call and a delayed reaction of the US and international funds.

The sovereign risk premium before the recent geopolitical events averaged 10% based on the USDRUB oil ratio and now exceeds 20-23% based on a conservative estimate, taking into account the long-term geopolitical risks which are permanently associated with the Russian assets. The country risk premium across all Russian asset classes averages 25%. The rouble’s strengthening to at least ₽65/$ at the current oil price is justified if the situation de-escalates (see table below).

Our base case scenario is contrary to investors’ fears and assumes de-escalation, no additional sanctions against Russia and diplomatic agreement that will lead to market rebound back to pre-selloff levels of October 2021 and higher. Prior to the escalation on October 26, 2021, when Brent oil traded at $86/bbl, the USDRUB was below ₽69/$, Gazprom and Sberbank traded ₽370/share with sanctions risks and geopolitical premium at the time. Oil is now approaching $90/bbl and is likely to reach $100/bbl by the end of the quarter on the back of strong demand in Asia and limited supply from exporting countries, and recent tactical factors such as a drone attack on oil storage facilities in Saudi Arabia.

We assume that chances of mild sanctions like sanctions against Russian banks that will also be market supportive leaving room for postponed/delayed diplomatic talks stand at 30% and tough sanctions at 10%, that is sanctions against the president, sanctions related to exclusion of Russia from SWIFT and economic embargo which is interrelated and hence permanent cut in diplomatic relations between Russia and the West that will not just lead to massive Russian assets dislocation but globally as well especially with respect to commodities.

Potential mild sanctions

Mild sanctions will concern sanctions and penalties against large Russian banks. We believe on top of the list is Promsvyazbank due to its ties to Russian military and defence spending, other financial institutions that are on the US monitoring list but are not sanctioned yet are SOGAZ, Bank Otkritie.

Moscow credit bank (MCB) is not on the list but could be the new target due to its affiliation with Rosneft. We assume that banking sanctions do not assume extension of sanctions to at least Sberbank and VTB due to the dominant share of retail deposits and given that they are already under sectoral sanctions, but sanctions could be extended to VEB, Gazprombank or Rosselkhozbank for example. Besides banks, corporates that could come under sanctions include Safmar, Rosatom and United Aircraft Corporation. We assume that sanctions on banks would primarily target access to foreign capital markets and perhaps more restrictions (debt and equity transactions and other restrictions for international counterparties) as was the case with Sberbank, VTB, Rosselkhozbank, VEB and Gazprombank in the summer of 2014 and overall they had limited impact on banks revenue.

US sanctions are broken into three categories: SDN (Blocking) Sanctions, SSI (Debt and/or Equity) Sanctions and SSI (Oil Project) Sanctions. According to US initial sanction prerogative doctrine, most sanctions established by executive orders do not target the Russian state directly in social terms. Instead, they consist of designations of specific individuals, entities, vessels, and aircraft on the Specially Designated Nationals and Blocked Persons List (SDN) of the Treasury Department’s Office of Foreign Assets Control (OFAC).

Our targets for key Russian assets

When final sectoral sanctions were imposed by the end of September 2014 Russia 5yr CDS had reached 260 bps and as high as 223 bps on January 18. That means that most of the selloff in Russian 5yr CDS, OFZ, quasi-sovereign bonds in roubles and in FX and equities is overdone, implying potential pullback at least to beginning of Q421 and higher given huge lagging effect to oil and commodity prices.

Our base case, or mild sanctions against Russia, goes with the argument that the US is not looking for potential war conflict or harsh escalations, but wants to keep control over the Russian political elite and its affiliates. The West has exhausted much of the sanctions tools already, so it can expand the blacklist further, but is not going to cross the red line! Cutting Russia from SWIFT operations is the crossing of the red line and is similar to the oil and gas embargo since the bulk of transactions for oil and gas exports are done in USD. Out of total Russia’s exports more than 37%+ account for oil and around 13% for gas, hence there would be no settlements if Russia is cut off from SWIFT unless in other currencies or via barter. In this case, Russia and China will create a payment system alternative to that of the US, but how Europe will then pay for the Russian gas?!

Targets for key Russian assets

Source: ITI Capital, Bloomberg

Russia’s credit is better protected

2014 sectoral sanctions imposed by the US and the EU cost Russia $40 bln according to the country’s ministry of finance, but the overall price was higher due to an oil market slump and collapse of the rouble, CBR’s FX-reserves were down by $140 bln from $490 bln (Feb 2014) to $350 bln (March 2015) as a result of oil slump and CBR FX-interventions. Oil prices dropped from $112/bbl (Feb 2014) to $31/bbl (Jan 2016).

Now the situation is reversed, Russia has record high FX and gold reserves of $630 bln, low external debt ($472 bln down from $728 bln back then) and benefits from surging oil prices approaching the highs of Q314.

What does the performance of Russia’s CDS tell us?

CDS, credit default swap, reflect the cost of insurance against Russian sovereign bonds default. It is essentially a measure of the risk for non-residents and therefore CDS primarily reflect the concerns of major Western funds and reflect a combination of factors, rather than a single factor that might affect one particular asset. The higher the CDS, the higher the cost of risk insurance and hence the greater the probability of default.

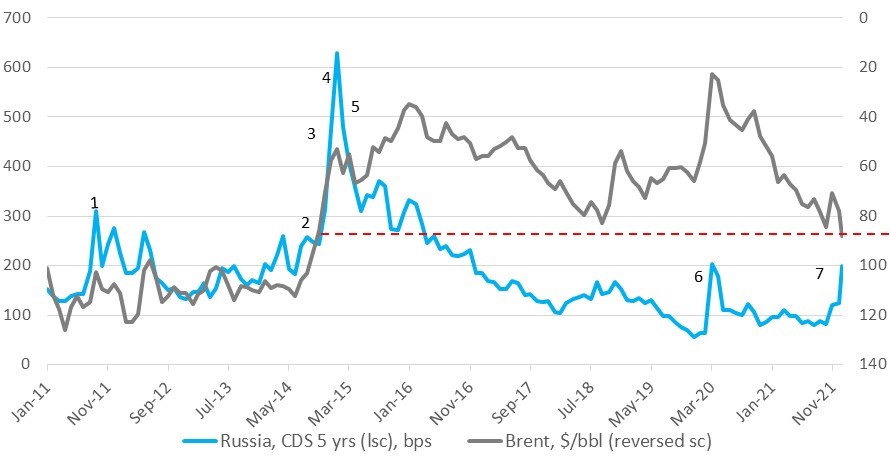

Graph Worth a 1000 Words

Source: ITI Capital, Bloomberg

1. June 2011-September 2011, 5yr CDS spiked by 200 bps due to government reshuffle, dismissal of finance minister Alexei Kudrin, CBR’s sanation of Bank of Moscow, a surge in Russia’s government borrowing and a slowdown in global economic growth amid external volatility.

2. Feb/March 2014 Crimea annexation, July/September 2014 US sectoral sanctions against Russian companies and banks.

3. Oil prices dropped from $112/bbl (Feb 2014) to $47/bbl contributing to losses in Russian CDS amid huge USDRUB volatility. From February 2014 - January 2015 Russian 5yr CDS jumped by 437 bps to reach an all-time high of 629 bps.

4. CBR FX reserves depletion, from Feb 2014 to March 2015 CBR’s FX-reserves dropped by $140 bln, out of which half was used for CBR interventions to support the rouble. In December 2014, the US imposed sanctions on Crimea, and in February 2015 the EU expanded the Russian sanction list by adding 151 individuals and 37 entities. USDRUB rose by 50% from October 2014 to February 2015.

5. Oil prices fell further to as low as $31/bbl in January 2016 and then started to recover, boosting confidence in Russian assets as geopolitical tensions began to ease after sanctions.

6. Global financial meltdown due to covid19 outbreak and oil prices collapse by >70%

7. Russia-Ukraine-NATO-US-Europe new geopolitical tensions amid global commodity boom.