ITI Capital: Jaguar Land Rover 23" и 24" – highest euro and pound yielders amongst automakers

Рынок Акций

Рынок Облигаций и Валюта

JLR cross currency trade recommendation: BUY Jaguar Land Rover (JLR) EUR- and GBP-denominated securities against JLR USD-denominated bonds

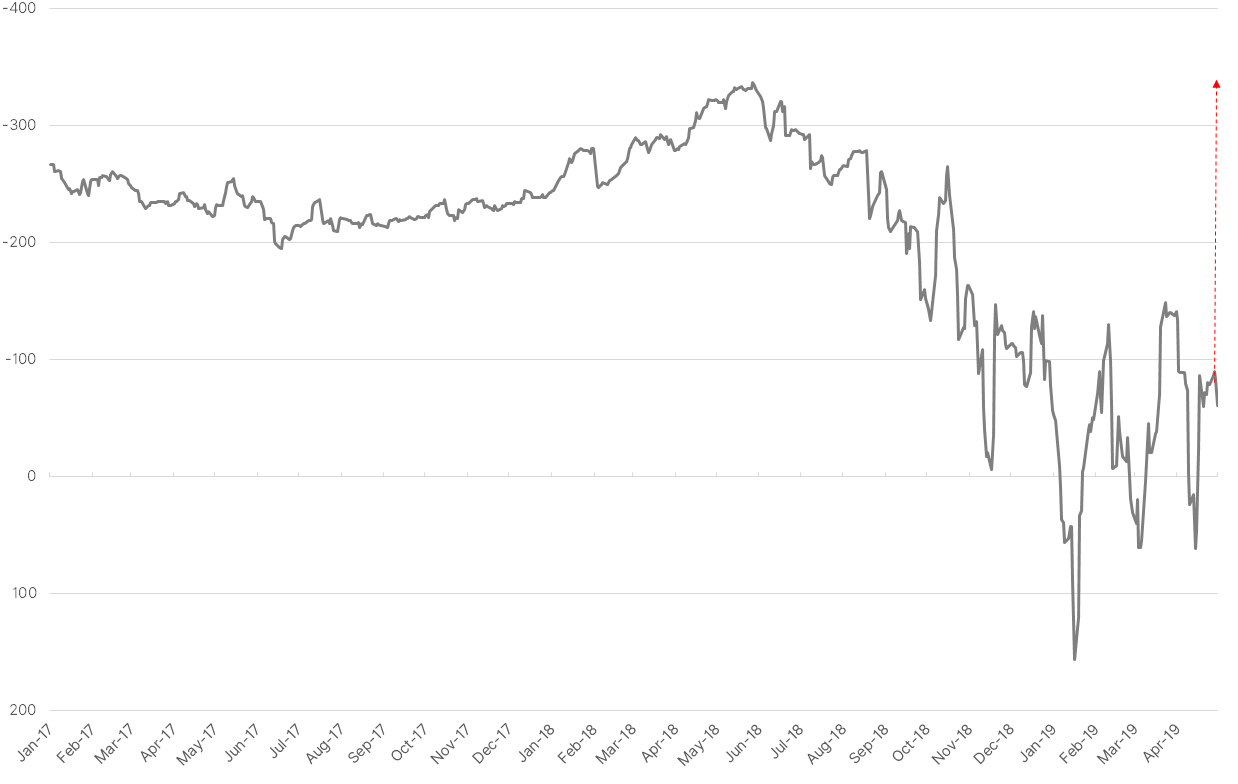

- The current spread between euro issues maturing in 2024 and similar dollar issues stands at −86 bps. The spread between JLR euro-denominated and dollar-denominated bonds has been −220 bps over the past two years. Traditionally, YTM in EUR is significantly lower than of the same security in USD due to the difference in the key rates. For example, the coupon for euro-denominated JLR bonds maturing in 2024 stands at 2.2% against 5.75% for that of dollar bonds with similar maturity

- Therefore for EUR-denominated issue maturing in 2024 we expect spread narrowing by additional 130 bps. This, in turn, implies the prices surge by 5.7%, to 93.5%, and a yield drop to 3.75%

- With respect to GBP-denominated issues with maturity in 2023 and a 3.875% coupon looks even more appealing against dollar-denominated issues with a 5.75% coupon. The spread for the issue in pounds is even wider than that in euro and amounts to −122 bps, implying a potential yield decline by 160 bps to 5.2%, and the price increase by 5.6% up to 95.5%

Our recommendations

Spread between euro-denominated and dollar-denominated bonds

Source: Bloomberg, ITI Capital

Investment case

- As of 2018, Tata ranked 21st largest car producer after SAIC Motor. The company ranks 18th year-to-date: 215,000 cars, the market share just over 1%

- In February 2019, TataMotors surprised the market by posting the biggest-ever quarterly loss in Indian corporate history of about £4 bln. The group decided to cut 4,500 jobs as part of its cost efficiency plans. Since November 2018 till February 2019, euro-denominated bonds prices have dropped by 25 pp to 76%, while yields have surged by 400 bps to 8%, resulting in a widening of the spread between euro- and dollar-denominated bonds to +150 bps. Since then the spread has narrowed and turned negative, but lags way behind a fair level. Interestingly, the yields of bonds in dollars have mostly recovered to November levels, in contrast to euro yields as a result of BREXIT fears and other factors

- Based on the highest price of JLR bonds in euros and in pounds for the past 12 months, the price upside potential is over 10%

- We believe that the yields of bonds in euro should be lower (as is usually the case), based on the spread between the borrowing curve in euros and in dollars.

- The yields of bonds in euro is the highest amongst car producers

China’s car market is recovering following a disastrous start of the year

- JLR posted $152 mln adjusted net profit for the three months ended March 2019 due to stronger sales in the US and UK. The company reports encouraging demand for new models and is on track for further growth

- The recent comments from Tata Motors CFO (JLR’s parent company) make JLR bonds even more appealing. JLR China sales should return to growth «a quarter from now,» Tata Motors’ Chief Financial Officer P.B. Balaji told reporters in Mumbai, reiterating the Indian company wasn’t looking to sell its luxury cars unit

- JLR China sales for March surged 70% to 2.3 mln units following a record slump in February when the figure hit the lowest since June 2011. Eurozone sales jumped by 52%, although globally they continue to fall, in March they declined by 12% mom, to 6.2 mln units. China and the eurozone account for 43% of all JLR sales. The current dynamics suggest that the worst was over for JLR in the late 2018

Good credit makes JLR look attractive

- Currently, there are 10 outstanding JLR bond issues totalling $4.6 bln divided equally between pounds and euro

- What is relevant to us is two issues in euro and pounds with an average duration (less than seven years) against similar issues in dollars. The latter have materially recovered following a slump in late 2018 due to a record £3.1 bln loss in the company’s history, that contributed to a record loss for the entire Tata Motors Group. Tata snapped up JLR from Ford Motor in 2007 in June 2008, shortly before the crisis set in. Ford bought Land Rover from BMW in 2000

- JLR accounts for a big share in Tata’s consolidated revenue

- JLR’s total debt, including credit lines, is $5.7 bln, including $2.5 bln of debts that can be refinanced/renewed

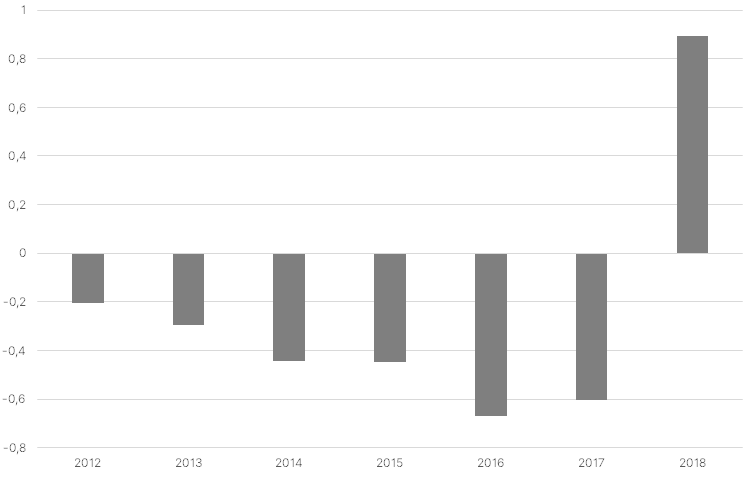

- Thus, JLR’s total net debt as of 2018 was only $813 mln, net debt/EBITDA is below 1x, implying strong credit reliability

Net Debt/EBITDA ratio

Source: Bloomberg, ITI Capital

Positive triggers

- Low Net Debt/EBITDA ratio <1x

- Jaguar Land Rover announced all its vehicles will be available in electric or hybrid models from 2020, giving their customers even more choice

- Support from Tata Motors (parent company)

- China sales growth in March

- Prospects of trade agreements between the US and China

- Lifting of tariffs on car imports from Canada and Europe

- President Trump agreed to lift tariffs on metal imports from Mexico and Canada

- Trump postpones tariff decision on car imports for six months to reach agreement with Japan and EU

Key risks

- No-deal Brexit will cost the company over £1 bln in annual profit

- Global economic slowdown and further decline in car sales

- Escalation of trade spat and higher tariffs on cars and components/spare parts

- JLR believes sales have been hurt by the shift away from diesel in Europe, where 84 percent of JLR’s vehicles are sold with the powertrain

Euro-denominated bonds yields map, %

Source: Bloomberg, ITI Capital